Related Blogs.

IR35: Challenges for the construction industry

Construction was one of the first industries to open up after the first Coronavirus lockdown, with the government hailing the critical efforts of construction workers and businesses at the time.

This was an enormous undertaking for the industry, having to change working practices to make sites Covid-safe and keep operations going with many workers on furlough.

In 2021, construction faces a new challenge – reform to the IR35 off payroll tax rules.

Shift in responsibility for IR35

Changes to the way IR35 is applied were first introduced in the public sector in 2017. The roll-out of these rules to the private sector was due to be implemented in April 2020, but was delayed by a year due to the pandemic.

IR35 is designed to catch “disguised employment”. It basically says that where a worker is supplying services through a limited company, but to all intents and purposes is working in the same way as an employee, they should be taxed as an employee.

Come 6th April 2021, the key difference is that it becomes the responsibility of the end user to identify which services are caught by IR35, and ensure that payment for those services is treated as employment income for tax purposes.

This shift will apply to all large and medium sized engagers across the private sector, but what are the particular challenges for the construction industry?

Construction supply chains

Construction businesses often use many tiers of sub-contractors to complete a project, and that’s where things get complex in terms of IR35.

Under the new rules, it will ultimately be the responsibility of the end user to:

- Determine the employment status of each individual on a project, whether that is self-employed, employed or “deemed employed”

- Ensure that where a worker is “deemed employed” ie. caught by IR35, they are paid PAYE by the free-payer in the supply chain, which may be the agency that provided that worker.

Where a worker disagrees with an IR35 decision

A further challenge for the construction industry is that there are many trade specialists who have been supplying their services through their limited companies for years, and may not agree with the end user’s assessment of their employment status for a particular contract.

The end user, as well as being obliged to communicate employment status up the supply chain, also has a duty to deal with appeals to the decision within 45 days of the work raising an objection.

Systems and processes will need to be in place to document the employment status decision and allow appeals to be made and responded to within the mandated time.

Paying “caught” workers

Finally, comes the question of how to pay workers who are assessed as caught by IR35 and “deemed employed” for tax purposes.

This is the responsibility of the fee-payer, so will be a challenge for recruitment agencies in the construction sector, however it should be noted that the end user still carries risk, as liability can be passed up the chain.

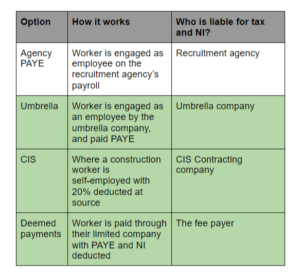

IR35 compliant payroll options

Liquid Friday and our partners can deliver all of the “green” payroll options above, and provide help and support on IR35 for contractors, agencies and end users.

Join our IR35 webinar

We will be running a series of agency-specific webinars on IR35 throughout February.

Join our panel of industry experts who will walk you through IR35, what it is, why it matters and what you need to do to prepare for the reforms in April.

We promise it won’t be too heavy and you will come away knowing more than when you joined.

Click here to book your place.